Open enrollment season is just around the corner, and understanding your health insurance options is essential in order to make informed decisions. To help you navigate the various plan types and networks available, we’ve compiled a list of essential benefits terms and explanations which should help you decode a few acronyms before open enrollment arrives. Whether you’re choosing a new plan or just want to better understand your current one, this guide will equip you with the knowledge you need to get started.

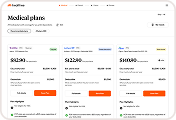

Benefits Payments

There are five main types of payments related to insurance coverage. These terms are some of the most important to know:

- Premium: The amount you pay every month for your health insurance, kind of like a subscription.

- Deductible: The amount you pay out-of-pocket each year before your insurance starts to cover costs. So, if your deductible is $1,000, your insurance plan will only begin paying for certain services after you’ve spent $1,000 that year.

- Co-pay: A fixed amount you pay for specific services, like a doctor’s visit, similar to a service fee.

- Co-insurance: The percentage of costs you pay after meeting your deductible, like splitting the bill with your insurance.

- Out-of-pocket maximum: The most you’ll have to pay in a year; after reaching this, your insurance covers 100% of covered services.

Accessing Care

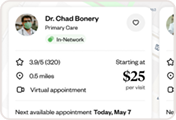

- Primary Care Physician (PCP): Your main doctor who manages your overall health and may refer you to specialists for specific issues.

- Referral and Pre-authorization: A referral is permission from your primary care doctor to see a specialist. Pre-authorization is approval from your health plan for certain services before you receive them.

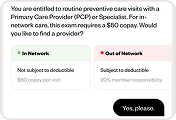

- In-network and Out-of-network: In-network providers have agreements with your health plan to offer services at lower rates. Out-of-network providers do not, usually resulting in higher costs for you.

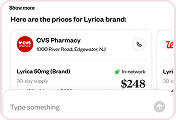

- Healthee: A web platform and app where you can easily compare healthcare providers based on cost, location, and coverage. Ask it questions and it helps you manage your healthcare needs efficiently.

Types of Care

Different types of healthcare services are covered differently by health insurance plans. To find services you are covered for, just check your Healthee account.

- Preventive care: Services like check-ups, vaccinations, and screenings that help prevent illnesses. Most health plans pay for these services in full, so be sure to take advantage of them.

- Emergency care vs. Urgent care: Emergency care is for emergencies that require immediate attention, such as a wound or broken bone. Urgent care is more for minor injuries or minor illnesses.

- Specialist care: Specialized care for your joints, eyes, skin, digestion, or any other specific health concern. May require a referral from your main doctor.

- Therapeutic care: Physical therapy, occupational therapy, and speech therapy for recovery and rehabilitation.

- Telehealth: Allows you to consult with healthcare providers by phone or video.

- Mental health care: Therapy, counseling, and treatments for psychological and emotional well-being.

- Chronic care management: Ongoing care for chronic conditions like diabetes, asthma, or hypertension.

- Pediatric care: Healthcare services for children.

- Palliative and Hospice care: Supportive care for serious illnesses, focusing on comfort and quality of life, often at the end of life.

Benefits

- Formulary: A list of prescription drugs covered by your health plan.

- Explanation of Benefits (EOB): A statement from your health plan showing what was covered for a medical service and what you owe.

- Claim: A request submitted to your health plan, either by you or your healthcare provider, to pay for services.

- Health Savings Account (HSA) and Flexible Spending Account (FSA): Both are special accounts you can use to save money tax-free for medical expenses. HSAs carry over from year to year, while FSAs do not — so be sure to spend your FSA money before it disappears.

Understanding Plan Types

Health Maintenance Organization (HMO)

An HMO is a popular choice for those who prioritize preventive care. These plans typically offer lower costs by working with a specific network of doctors, hospitals, and specialists. To receive covered services, you’ll generally need to stay within this network, except in emergencies. Your primary care physician (PCP) will be your main point of contact for medical care, and you’ll need a referral from them to see specialists.

Preferred Provider Organization (PPO)

If you value flexibility in choosing healthcare providers, a PPO might be the best option for you. PPOs allow you to see any doctor or specialist you wish, even those outside your network, though staying within the network will save you money. One of the biggest perks is that you don’t need a referral to see a specialist, making it easier to get the care you need when you need it. However, this flexibility often comes with higher premiums and out-of-pocket costs.

Exclusive Provider Organization (EPO)

EPOs offer a balance between cost and flexibility. Like an HMO, an EPO requires you to stick to a network of providers for non-emergency care, but you don’t need a referral to see a specialist. This can be a cost-effective option if you’re comfortable with the providers in your network.

High Deductible Health Plan (HDHP)

HDHPs are known for their lower monthly premiums, but they come with higher deductibles. This means you’ll pay more out of pocket before your insurance starts covering costs, except for preventive care, which is fully covered. HDHPs often pair with Health Savings Accounts (HSAs), allowing you to save pre-tax money for future medical expenses. You also have the flexibility to see specialists without needing a referral.

Reference-Based Pricing (RBP)

With an RBP plan, you have the freedom to choose your healthcare providers, but your insurance will only cover services up to a set reference price. If the provider charges more than this amount, you may need to negotiate the price or pay the difference yourself. Some plans offer assistance with negotiations, so it’s a good idea to reach out to your plan’s customer service for support.

Indemnity Plan

Also known as a fee-for-service plan, indemnity plans offer the most freedom in choosing healthcare providers. You can see any doctor or specialist without a referral, but you’ll typically need to pay for services upfront and then submit a claim for reimbursement. The plan will cover costs based on “usual and customary charges” for your area, so it’s important to be aware of what providers typically charge.

Decoding Network Types

Traditional Network

A traditional network includes a specific group of healthcare providers, such as doctors, hospitals, and specialists. Staying within this network is crucial for keeping your healthcare costs down. Most traditional networks also offer coverage for out-of-network care in emergencies.

Multi-Tier Network

Multi-tier networks categorize providers into different levels, or tiers, based on cost or quality. You can save money by choosing providers from preferred tiers, but you’ll still have the flexibility to see providers in other tiers at a higher cost.

Multi-Network System

Multi-network systems give you access to multiple networks of healthcare providers. This arrangement allows you to enjoy the cost savings associated with network care while also benefiting from a broader range of provider options.

Open Network

An open network gives you the freedom to see any healthcare provider without restrictions. This flexibility can be beneficial, but it usually comes with higher out-of-pocket costs, so it’s important to weigh your options carefully.

Point of Service (POS) Network

POS networks combine elements of HMOs and PPOs. You’ll need to choose a primary care physician and get referrals to see specialists. However, POS plans also cover some out-of-network care services, though at a higher cost.

In Conclusion

Understanding these key terms can empower you to make the best decisions for your healthcare needs during open enrollment. Take the time to review your options, consider your health priorities, and choose a plan that provides the coverage and flexibility that’s right for you.